Acute shortage of inputs and higher logistics costs affect machinery manufacturers’ margins

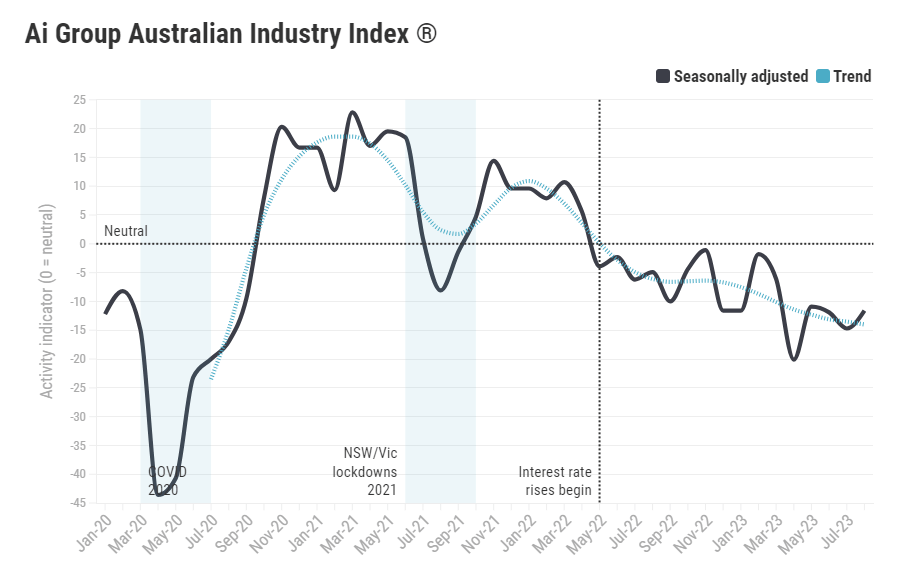

Australia’s downstream manufacturing sector – including machinery and equipment – contracted in August, according to the Ai Group Australian Industry Index.

Released last week, the machinery and equipment sector index dropped by four points to be broadly stable (-1.2).

The food, beverages and TCF sector fell strongly, to be well into contractionary territory at -18.5.

Ai Group says a lack of suitable inputs is acute for machinery manufacturers, while higher logistics cost continued to affect margins.

Food and beverage firms reported increased competition in a market where growth has slowed due to sluggish consumer demand.

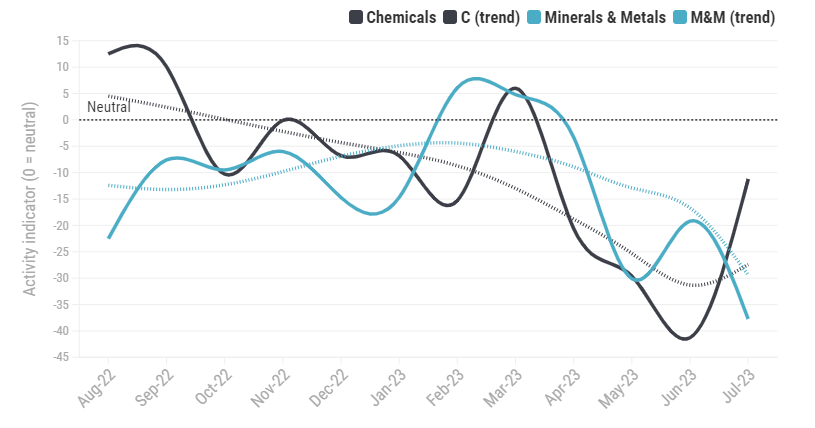

Upstream manufacturing indicators moved in different directions in August, but all remain in contraction.

Chemical manufacturing declined again, by 4.3 points, to -15.5. The minerals and metals industry rebounded significantly, rising 17.3 points, albeit to -20.4.

August continued to be a weak ordering month for upstream firms, who also reported inability to recruit new workers due to higher wage rates.

Additionally, upstream manufacturers experienced a decreased sales enquiries due to lower supply constraints.

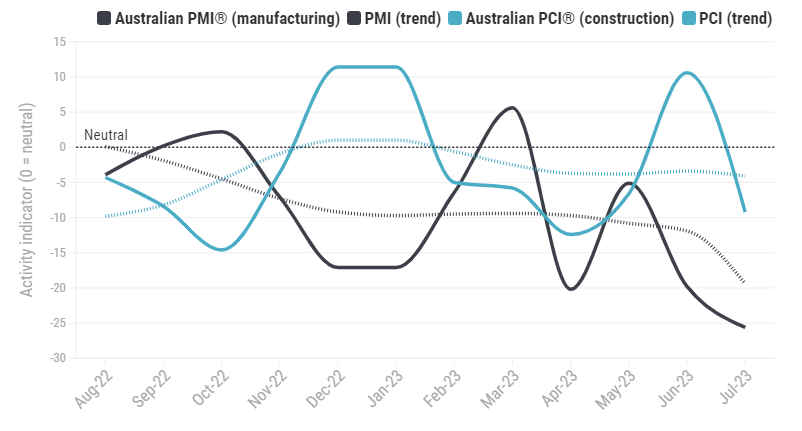

The broader Australian PMI (all manufacturing) grew by 5.8 points but remains in contraction (-19.8); while the PCI (construction) declined slightly by 0.7 points, and remained in negative territory (-9.9).

Survey respondents reported continuing difficulties in recruiting suitable people for vacant positions and obtaining reliable overseas suppliers.

Construction industry players reported cautiousness due to high interest rates leading to a period of quiet building demand.

Including business services, which remained in contraction (-10.1) despite a slight rise of 4.9 points in August, the headline Australian Industry Index indicated contracting conditions in August, for the sixteenth month since the start of the current interest rate rising cycle.

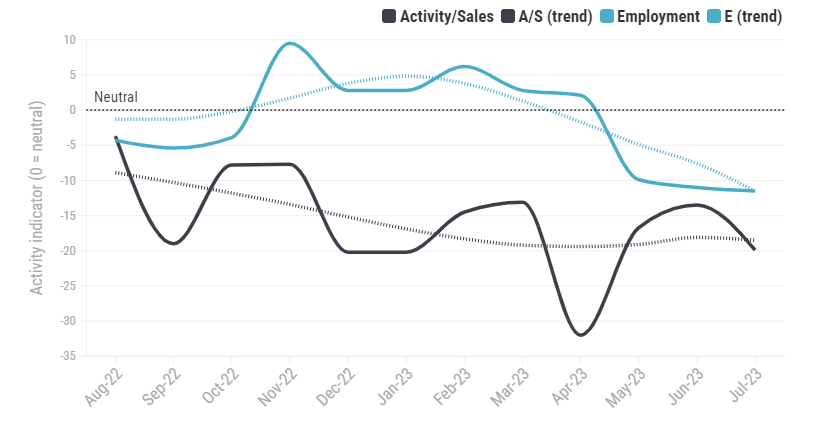

The employment, industrial activity and new orders indicators all continued to indicate contractionary conditions.

Input prices eased, while input volumes grew into expansionary levels not seen since mid-2021. This suggest supply chain pressures are continuing to soften.

Price indexes all fell in August, reflective of lower but still persistent inflation. The sales price indicator fell to its lowest reading (+6.5) since the height of the pandemic in mid-2020.

The activity/sales indicator continued to dip mildly in August, falling by 0.8 points to indicate broader contraction at -20.7.

The employment indicator recovered slightly in the month yet still remained in contraction (-9.2). The indicator remains in territory last seen during the height of the pandemic.

Some survey respondents pointed to weak sales as a factor behind contracting activity and employment.

The decline in new orders eased after falls in June and July, but it remains in contraction at -18.0 points. The new orders indicator has been negative for six months, since February 2023.

All pricing indicators eased in August, consistent with slowing inflation. The input price indicator fell by 13.2 points while sales price followed this trend and dropped by 14.2 points.

The gap between the input and sales price indicator slightly widened again, suggesting an ongoing price squeeze on industry.